Letters From Larry is brought to you by our friends at YCharts. Exciting times at YCharts — they just announced their latest product enhancement called Proposals. YCharts Proposals is a game-changing capability, empowering wealth management professionals with the prowess to craft captivating narratives, effectively conveying their investment strategies that help win new business. But that's not all – mark your calendars for September 22nd because YCharts will be hosting a webinar to unveil Proposals and show off its full potential. You’ll learn how to whip up reports that don't just highlight the value of your investment strategies but also cater to your clients' unique financial needs. Click the link in the show notes to register for YCharts’ webinar if you want to learn more about Proposals, and get 15% off your initial subscription when you start your free YCharts trial (new customers only)

Note to Public Readers from Larry: September’s difficult seasonality doesn’t disappoint, and our proactiveness means that this month provided us another window of opportunity to build on our alpha against the S&P 500. Markets have retraced about 60-65% of last week’s advance but ends the week on a more solid footing. I do think we stabilize a bit for a few sessions before Sellers re-emerge.

Key Investing Resource: Strategist Larry uses Interactive Brokers as his core brokerage. Feel free to check out IB. I currently park excess cash at Interactive Brokers. Check it out. It’s a great brokerage.

In our emails, we will provide the following coverage points:

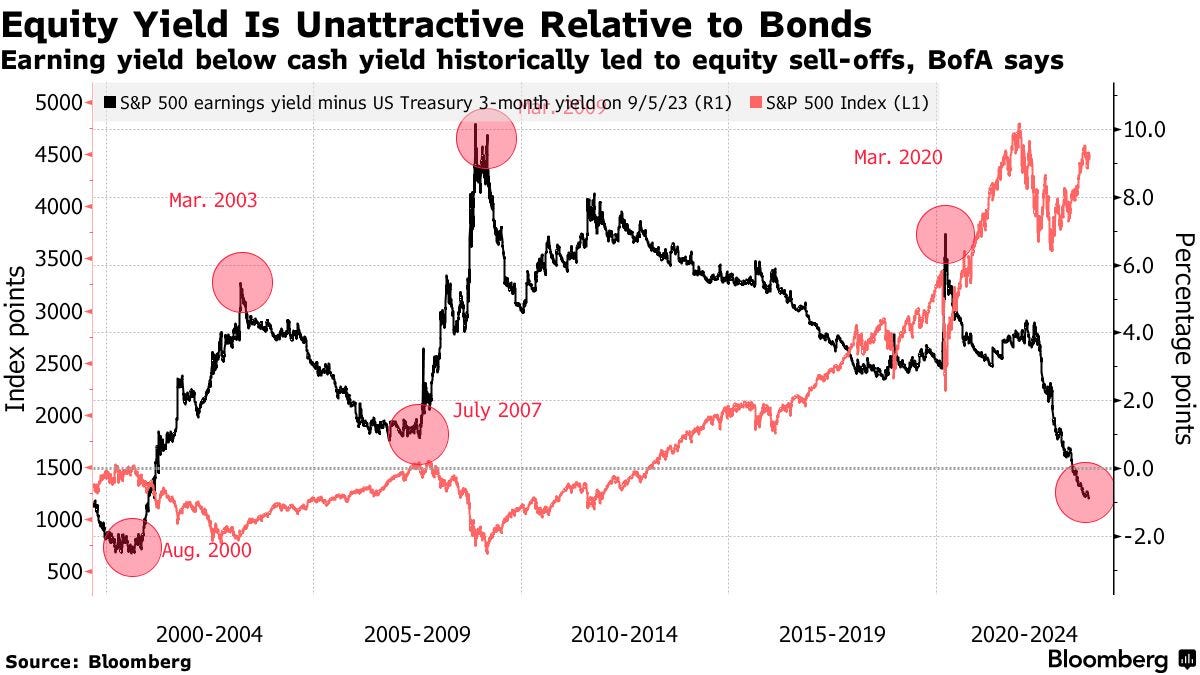

Rising bond yields are making stocks less appealing, evidenced by the S&P 500's earnings yield of 4.6% being overshadowed by the three-month Treasury bill yield of 5.5%. This negative difference of -0.9% is the largestsince 2000. Historically, wide positive differences between earnings and bond yields have favored stocks and credit, as seen in March 2003, 2009, and 2020. However, when the difference turns negative, like in August 2000, or narrows significantly, as in July 2007, risk assets like stocks tend to underperform.

Macro Chart In Focus

Analyst Team Note:

Data from the US Treasury shows a significant increase in receipts for the Department of Education (DoE), with a rise to $6.4bn in August from $2.1bn in July and $1.2bn in June.

This is likely attributed to a resumption in student loan repayments, which came sooner than anticipated.

Initially, repayments were expected to rise in October, with a gradual return to pre-pandemic trends. However, the early surge in August implies that borrowers have adjusted well to the repayment resumption, signifying minimal impact on future consumer spending. The effect on spending due to these repayments will be more immediate than previously thought.

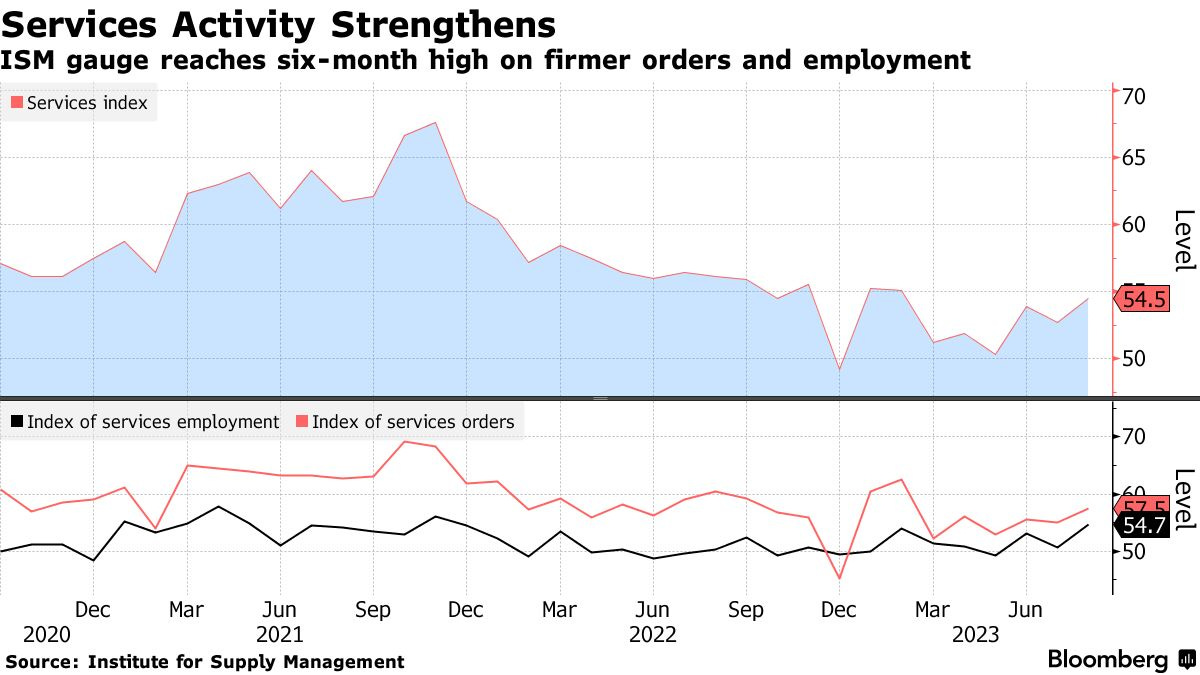

US service sector activity reached a six-month high in August, driven by a rise in new orders and employment.

13 service industries, including real estate and food services, reported growth. In addition, the ISM employment index reflected increased hiring. However, there were concerns as material and wage costs rose, potentially prolonging high inflation.

ISM also recorded an uptick in new orders, higher business activity, and rapid export growth. Various sectors shared their insights, highlighting positive trends in restaurant sales, stability in hiring, strong national sales in construction, and the return of material availability to pre-pandemic levels.

However, challenges such as high pharmaceutical costs impacting healthcare margins and rising interest rates slowing residential construction were noted. Despite the generally positive outlook, a worrisome increase in inventories and concerns about high stockpiles could lead to future reductions in orders with manufacturers or other service providers.

Chart That Caught Our Eye

Sentiment Check

Make sure to check Larry’s most recent market updates via his personal newsletter.