8.3.22: An extreme push to deny the Recession Narrative via higher stock prices

Key U.S. and China brief market notes by Larry's Analyst Staff Team.

Note to Readers: While Strategist Larry believes there are selective areas of value in the stock market, much of the latest advance has closed any valuation discounts that were available just 30 days ago, a reminder of how much can change in just one month (on the upside or on the downside).

He issued a buy on Semiconductors (SOXX/AMD/NVDA/MU/AMAT/LRCX) and a Hold/Risk-Reduction on China in his July Investment Research Report. He also viewed the S&P 500 potentially staging a counter-trend rally into the 4000-4200 region. That thesis has played out. Moving onto August, it would be in your best interest to understand his views on the Chinese Internet Sector and the S&P 500 now that valuations have been recalibrated.

Do not miss this opportunity to protect yourself from what could end up being a deadly bull trap later this Summer/Fall. We are evaluating this possibility every single day with our fundamental, macro, and technical work to take advantage of whatever upside is left.

While we cannot know for certain when the current counter-trend rally breaks, we do NOT want you to be the exit liquidity for institutional investors.

This email is brought to you by Interactive Brokers, one of our preferred brokerages to buy HK-Listed Shares in our China Internet Equity Coverage Universe.

In our emails, we will provide the following coverage points:

Brief Snapshot of U.S. & China markets and valuation

Our Analyst Team’s Chart in Focus

U.S. & China Upcoming Economic Calendar Snapshot

Notable Chart from Media Outlets

Fear & Greed Index Recap

I hope you find this newsletter to be insightful and enjoyable! - Larry and Team

U.S and China Markets Brief Snapshot 🇺🇸 🇨🇳

(Powered by our Channel Financial Data Provider YCharts)

S&P 500 Index: 4091.19

KWEB (Chinese Internet) ETF: $28.12

Analyst Team Note:

Lots of news about Nancy Pelosi’s historic visit to Taiwan, which could likely lead to one of the most intense periods of military activity in the region.

The broad direction and impact on macro and markets is clear: assets exposed to China/Taiwan tension will likely warrant a higher risk premium over the coming weeks, while deteriorating US-China relations will accelerate decoupling, increasing pressure on Chinese ADRs as well as the global semiconductor and electric vehicle industries.

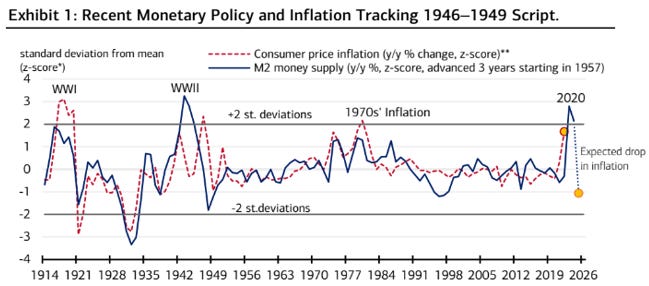

Macro Chart In Focus

Analyst Team Note:

Incredible note from BofA today…

“While the equity market turned exuberant when Fed Chair Powell suggested that rate hikes could moderate or even stop in the year ahead, money growth will likely fall dramatically if QT continues as planned, financial conditions will continue to tighten, and the dollar will keep strengthening.

In fact, as currently projected, the monetary-base shrinkage over the next year would be unparalleled, and the dollar shortage this would create in a heavily dollar-indebted global economy would put more and more strains on the global financial system until something would break. It would be unprecedented for the economy to bottom before the Fed stops removing liquidity from the system.”

Upcoming Economic Calendar

(Powered by our Channel Financial Data Provider YCharts)

U.S Economic Calendar (Upcoming Data Points)

China Economic Calendar (Upcoming Data Points)

N/A

Analyst Team Note:

The number of available job openings decreased to 10.7 million in June from 11.3 million in May, the biggest decline since April 2020.

Bloomberg notes that fewer openings likely mean the froth is being blown off inflated listings for openings as the economy slows down, not that demand for workers is dropping.

Goldman Sachs notes that the jobs-workers gap declined to 4.8m workers in June, a notable decline from its peak of 5.9m workers in March. This improvement in labor market balance suggests that wage growth could slow in the second half of 2022.

Chart That Caught Our Eye

Analyst Team Note:

The move lower in equity volatility remains puzzling given the same risk backdrop and indicators pointing to economic weakness going forward.

BofA Global Research suspects the large gap between MOVE and VIX signals an underpricing of recession risks by the stock market and expects to see the difference eventually narrow through higher equity volatility, especially as investors start to price in a slowdown in corporate earnings and economic indicators.

JPM believes a spike in rates volatility could be a catalyst to move markets lower especially if earnings season begins to disappoint and CPI comes in hotter than expected.

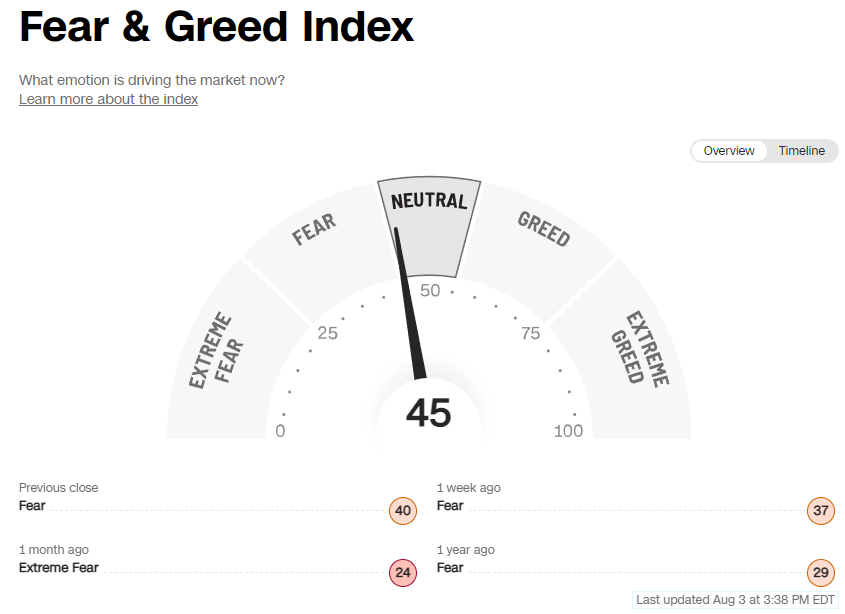

Sentiment Check

We want to take a moment to thank Interactive Brokers for being one of our Channel’s trusted Partners and to inform my audience of the special features they have given that our online friends here closely follow Chinese Internet stocks (BABA/Tencent).

Much of Larry’s audience is concerned about the US ADR issue of Chinese Stocks being delisted.

Interactive brokers allows investors to buy HK-listed shares of Alibaba, JD, Tencent, and other brand name Chinese Internet companies on the HK market. This will effectively reduce any confusion or work you will have to do in case there is the event of delisting US ADRs

Our Friends from Inside just said….