8.1.22: Complacency has returned to Investor Psychology

Key U.S. and China brief market notes by Larry's Analyst Staff Team.

Note to Readers: It’s a new month - we continue to look forward to helping you and our Community identifying opportunities and dangers. Take a moment to follow us on Social.

This email is brought to you by Interactive Brokers, one of our preferred brokerages to buy HK-Listed Shares in our China Internet Equity Coverage Universe.

In our emails, we will provide the following coverage points:

Brief Snapshot of U.S. & China markets and valuation

Our Analyst Team’s Chart in Focus

U.S. & China Upcoming Economic Calendar Snapshot

Notable Chart from Media Outlets

Fear & Greed Index Recap

I hope you find this newsletter to be insightful and enjoyable! - Larry and Team

U.S and China Markets Brief Snapshot 🇺🇸 🇨🇳

(Powered by our Channel Financial Data Provider YCharts)

S&P 500 Index:

KWEB (Chinese Internet) ETF:

Analyst Team Note:

The big question right now is whether we have bottomed of if we are in the midst of another bear rally. Here’s how these two scenarios could play out.

“We’ve formed a bottom” - Proponents of this view will point the economy having stalled but is likely to accelerate from here given we have passed the peak in inflation. The Fed is poised to reduce its hawkishness as inflation dissipates. Earnings are better than feared and that Q2 represents the low for the year. Light positioning and low liquidity will drive short covering first, then real buying, followed by increased leverage to longs. This could happen rapidly if the Fed actually pivots after the September meeting.

“Just another bear rally” - Proponents of this view will point to a rebound in commodities prices creating another leg higher, which could be exacerbated by the Russia/Ukraine conflict. Housing prices are likely to continue to move higher, albeit at a decreasing rate, as core inflation continues to surprise to the upside. The squeeze on the consumer will show up more aggressively in macro data creating several more quarters of low-to-no GDP growth. Further, we could see the Fed increase its hawkishness as both financial conditions and mortgage rates have come off their recent highs. Lastly, Q2 earnings could be the beginning of increased deterioration, triggering an earnings recession

Source: J.P. Morgan

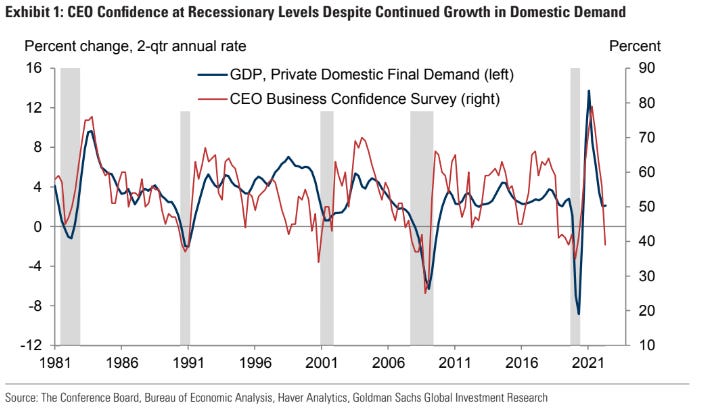

Macro Chart In Focus

Analyst Team Note:

After two negative quarters of GDP growth and a collapse in the CEO confidence survey, has the economy slowed beyond a healthy deceleration into outright contraction?

Corporate financial results and management guidance indicate otherwise: with nearly three-quarters of its market cap now reported, S&P 500 earnings have increased 9% year-on-year, 52% of reporters beat consensus expectations by 1 standard deviation, and revenues are growing in every sector.

Even excluding the outperforming energy sector, S&P revenues rose 3.8% in real terms, above the 2.6% average pace since 1970 and compared to an average decline of 1.2% in the first quarter of recessions (these data points are all preliminary, and note that many retailers report in August).

Credit market fundamentals are also reassuring: high-yield defaults are well below average.

Source: Goldman Sachs

Upcoming Economic Calendar

(Powered by our Channel Financial Data Provider YCharts)

U.S Economic Calendar (Upcoming Data Points)

China Economic Calendar (Upcoming Data Points)

N/A

Analyst Team Note:

Over the weekend, China’s official manufacturing PMI fell to 49 in July from 50.2 in June, signaling a contraction in activity. The economy’s recovery remains fragile as the government sticks to its strict Covid-Zero approach of tightening restrictions when virus outbreaks occur.

On the other hand, the Caixin manufacturing PMI, based on a survey of mainly smaller and privately-owned businesses, also showed weakening. The index dropped to 50.4 in July from June’s 51.7, missing the median estimate of 51.5 but staying above the 50 mark.

Goldman notes that there is sector coverage difference between the official PMI and the Caixin PMI. The official PMI covers more upstream sectors that are more energy-intensive while the Caixin covers more downstream.

Citigroup notes that the Chinese property market and fiscal policy are the top two areas for stimulus in the months to come. The government has been speeding up infrastructure spend and they believe that this could provide support for stabilizing the economy.

Sources: Bloomberg, Goldman Sachs, Citigroup

Chart That Caught Our Eye

Analyst Team Note:

Information tech experienced strong short selling momentum and was the most net sold sector on a global basis. If this bounce in the markets continue, we could see a squeeze and short-covering in Tech…

Source: Goldman Sachs Prime Services

Sentiment Check

Analyst Team Note:

After being stuck in “Extreme Fear” for a long time, we’re now approaching “Neutral”…

Stay cautious and disciplined.

We want to take a moment to thank Interactive Brokers for being one of our Channel’s trusted Partners and to inform my audience of the special features they have given that our online friends here closely follow Chinese Internet stocks (BABA/Tencent).

Much of Larry’s audience is concerned about the US ADR issue of Chinese Stocks being delisted.

Interactive brokers allows investors to buy HK-listed shares of Alibaba, JD, Tencent, and other brand name Chinese Internet companies on the HK market. This will effectively reduce any confusion or work you will have to do in case there is the event of delisting US ADRs

Make sure to check Larry’s most recent market updates via his personal newsletter. See you in our next update.