7.20.22: In our opinion, NFLX earnings foreshadow deeper problems with the state of the Consumer

Key U.S. and China brief market notes by Larry's Analyst Staff Team.

Note to Readers: We do not believe markets have bottomed, and we urge our readers to not chase in this counter-trend rally. Chasing this rally at this juncture may be met with regret (unless we see a surprise Dovish event at July FOMC). Our Community will provide the research on actionable strategy as retail investors get led into what we believe will ultimately be a bull trap. Price is one thing, value is another. Strategist Larry’s review of Netflix’s earnings report shows that the Consumer is more sensitive to price hikes than ever. In addition, their earnings forecast that they will return to subscriber growth before their ad-supported lower price tier launches in 2023 is a conclusion that is debatable. While broad market upside is of course still possible, at this point, we believe intermediate-term risk/reward to be against new long positions with SPX above 3970 (today’s local high). We will adjust our view if the Fed comes in significantly less Hawkish than we expect.

This email is brought to you by Interactive Brokers, one of our preferred brokerages to buy HK-Listed Shares in our China Internet Equity Coverage Universe.

In our emails, we will provide the following coverage points:

Brief Snapshot of U.S. & China markets and valuation

Our Analyst Team’s Chart in Focus

U.S. & China Upcoming Economic Calendar Snapshot

Notable Chart from Media Outlets

Fear & Greed Index Recap

I hope you find this newsletter to be insightful and enjoyable! - Larry and Team

U.S and China Markets Brief Snapshot 🇺🇸 🇨🇳

(Powered by our Channel Financial Data Provider YCharts)

S&P 500 Index: 3936.69

KWEB (Chinese Internet) ETF: $30.70

Analyst Team Note:

As Larry put it in his recent note to Patreon members, “[recent] price action is more of short-covering than organic buying demand. We are getting closer and closer to a level where I think LT bears will double-down on their efforts (again). Investor LT Larry thinks this environment is a hold. Tactical ST Larry is a bit more cautious. ST Larry will not chase today.”

Per Zero Hedge, market liquidity is still hovering at 5 year lows… Not much demand right now.

Macro Chart In Focus

Currencies as a % of Global FX Market

Analyst Team Note:

“Lingering geopolitical tensions, and their expected effect on eurozone growth, global recession fears and risk aversion in global markets are fueling USD strength.

De-globalization, the role of commodities as reserve assets and even the rise of digital currencies are often mentioned as denting USD dominance. The share of global FX holdings denominated in USD remains in the 60% ballpark, and this proportion has changed very little over the past 15 years.

The USD has benefited from demand for safety more than other traditional safe-haven assets in recent months. Positioning on the USD has been rising steadily since 2021, fueling the rise of the DXY to its highest level in over 20 years. The DXY has already benefited sharply from high risk aversion, but calmer waters on global markets are needed to ease the grip on the USD.” - UniCredit

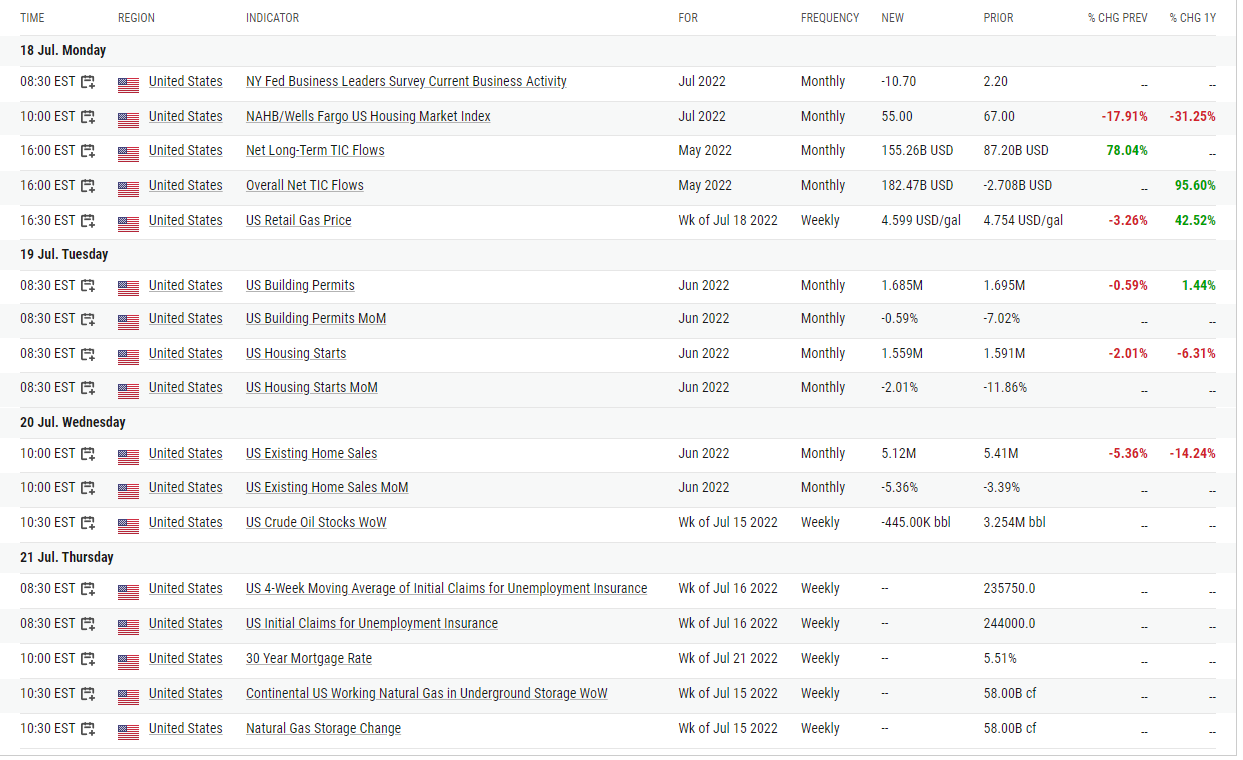

Upcoming Economic Calendar

(Powered by our Channel Financial Data Provider YCharts)

U.S Economic Calendar (Upcoming Data Points)

China Economic Calendar (Upcoming Data Points)

Analyst Team Note:

Bringing an overheating economy back into equilibrium requires some combination of improvements in the supply side of the economy and a sharp weakening of demand. The two most overheated sectors — labor and goods demand — remain too strong. Payrolls jumped another 372k in June, but need to slow to 100k or less. Retail sales are strong in nominal terms, but roughly flat in real terms. Further weakening in real retail sales would help unclog supply chains.

The supply-demand balance indicators remain troubling. May data still shows 1.9 job openings for every unemployed person. On the other hand, at least the unemployment seems to be leveling off at 3.6%. Finally, inflation news is mixed, with another ugly CPI report, but signs of weaker inflation expectations in the Michigan survey.

The bottom line of all of this is that the Fed still has a lot of work to do.

Chart That Caught Our Eye

Analyst Team Note:

Bank of America’s Global Fund Manager Survey yesterday gave a glimpse of how managers are thinking about the markets… The results weren’t pretty…

Expectations for global growth & profits at all-time lows

Cash levels at highest since September 2001

Equity allocation lowest since the fall of Lehman Brothers

Most crowded trades are in long US Dollar and long oil/commodities

According to BofA, “contrarian Q3 trade is risk-on if no Lehman, CPI down, Fed pause by Xmas...short cash-long stocks, short US$ - long Eurozone, short defensives-long stocks banks & consumer.”

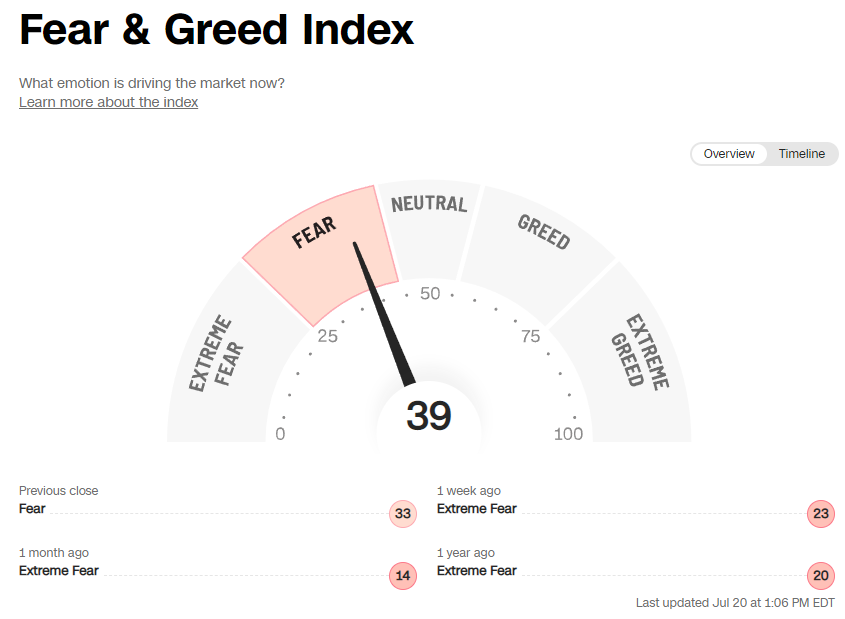

Sentiment Check

We want to take a moment to thank Interactive Brokers for being one of our Channel’s trusted Partners and to inform my audience of the special features they have given that our online friends here closely follow Chinese Internet stocks (BABA/Tencent).

Much of Larry’s audience is concerned about the US ADR issue of Chinese Stocks being delisted.

Interactive brokers allows investors to buy HK-listed shares of Alibaba, JD, Tencent, and other brand name Chinese Internet companies on the HK market. This will effectively reduce any confusion or work you will have to do in case there is the event of delisting US ADRs

Make sure to check Larry’s most recent market updates via his personal newsletter. See you in our next update.