7.15.22: The markets look past CPI Inflation. The true test comes soon.

Key U.S. and China brief market notes by Larry's Analyst Staff Team

Note to Public Readers/Members: Many people are very confused and torn whether this rally is the real deal as Inflation CPI surged to 9.1% for the June Print. We will be working this weekend to produce our July 2nd Half Report to answer this question with scenario analysis to help our Members plan for the coming weeks and months. We do not want you to miss the bottoming phase, nor do we want you to get stuck in a bull trap. Bull Traps are dangerous and this is what happened to Retail Investors who attempted to buy Alibaba north of 125/shr, which was precisely the range where we indicated caution & risk-reduction inside the Community.

Interactive Brokers is one of our Trusted Partners and has provided a stamp of approval on Larry’s Youtube channel for his high-quality investment research. IB is one of our preferred brokerages to buy HK-Listed Shares in our China Internet Equity Coverage Universe.

In our emails, we will provide the following coverage points:

Brief Snapshot of U.S. & China markets and valuation

Our Analyst Team’s Chart in Focus

U.S. & China Upcoming Economic Calendar Snapshot

Notable Chart from Media Outlets

Fear & Greed Index Recap

I hope you find this newsletter to be insightful and enjoyable! - Larry and Team

U.S and China Markets Brief Snapshot 🇺🇸 🇨🇳

(Powered by our Channel Financial Data Provider YCharts)

S&P 500 Index: 3790.38

KWEB (Chinese Internet) ETF: $29.45

Analyst Team Note:

As J.P. Morgan recently wrote in a note, “A few thoughts on growth and the market: TAMM is the new TAM – Try And Make Money”.

The market needs a shift in the narrative as it remains stuck in an endless negative feedback loop. We need to get through Q2 earnings to get a sense not just results but, more importantly, how Q3 and FY23 guidance looks and how that alters EPS estimates more broadly (though companies will likely feel discouraged from guiding optimistically). Going into Q2 earnings, remember that these companies are facing extremely challenging comps from Q2 2021.

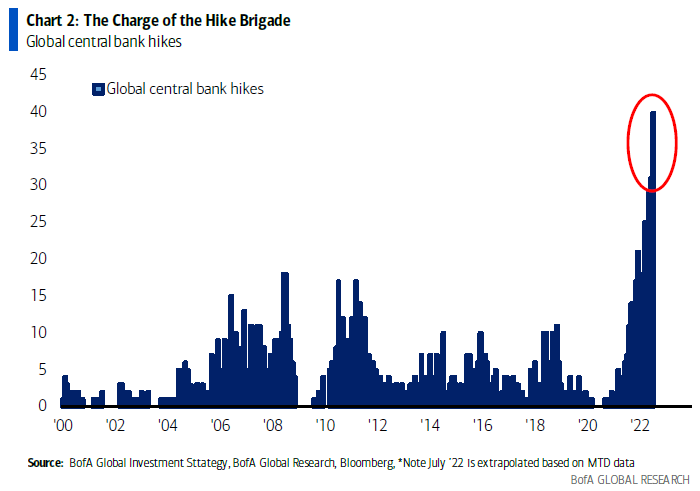

Macro Chart In Focus

Analyst Team Note:

Intense central bank hiking cycle could kill inflation but brings risk of a shallow (or deep) recession, which leads to pivot by central banks?

The issue here is that real policy rates are still so negative (-6.7% Fed, -8.8% ECB, -6.1% BoE, -2.5% BoJ). These big rate hikes as central banks play catch up in the coming months risks a credit event as the US dollar spikes to 20 year highs. Per BofA, spiking US dollar often portend credit events (1998, 2008, 2020).

While the Fed fund futures are pricing in rate cuts in 2H of 2023, some think the Fed will continue hiking in spite of growing cracks in the U.S./global economy. HSBC recently wrote “There has been too much attention paid to the USD’s frailties but not enough to the increasing challenges facing other currencies, which are contributing to the USD’s overvaluation. We believe that the Fed is far from done with hiking while global growth momentum is clearly deteriorating.”

Upcoming Economic Calendar

(Powered by our Channel Financial Data Provider YCharts)

U.S Economic Calendar (Upcoming Data Points)

China Economic Calendar (Upcoming Data Points)

Analyst Team Note:

Lots of housing data coming next week (permits, starts, sales, mortgage apps). Persistent supply constraints continue to pose headwinds to housing and additional rate hikes exacerbate affordability challenges, which could lead to a downtrend in demand. The biggest issue in housing right now is the supply demand unbalance.

On Thursday, initial jobless claims surprised to the upside with an increase to 244k in the week ending July 9 from 235k previously. This is the highest reading since November 2021 but claims are still at relatively low levels. As bad as it sounds, we need this number to continue increasing in order to bring more slack to the labor market.

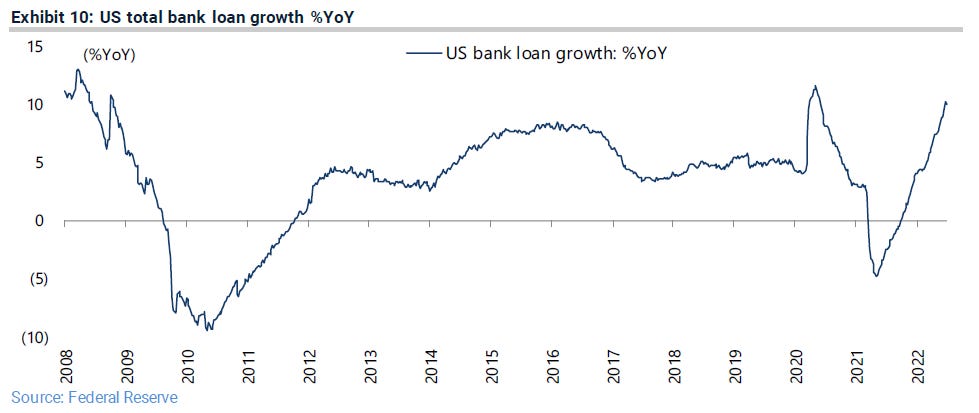

Chart That Caught Our Eye

Analyst Team Note:

“While reducing the Fed balance sheet via QT will reduce the Fed’s contribution to broad money supply, commercial banking can theoretically increase its contribution to broad money supply by increasing lending. This is why it is important to be aware of the continuing pickup in US commercial bank lending, however counter-intuitive this might be in the face of growing evidence of a slowing economy. Total bank loans rose by 10.0% YoY in the week ended 29 June and are up 15.5% on a 13-week annualised basis.” - Jefferies

Sentiment Check

We want to take a moment to thank Interactive Brokers for being one of our Channel’s trusted Partners and to inform my audience of the special features they have given that our online friends here closely follow Chinese Internet stocks (BABA/Tencent).

Much of Larry’s audience is concerned about the US ADR issue of Chinese Stocks being delisted.

Interactive brokers allows investors to buy HK-listed shares of Alibaba, JD, Tencent, and other brand name Chinese Internet companies on the HK market. This will effectively reduce any confusion or work you will have to do in case there is the event of delisting US ADRs

Make sure to check Larry’s most recent market updates via his personal newsletter. See you in our next update.

Words of Affirmation from inside our Community