Key Investing Resource: Strategist Larry uses Interactive Brokers as his core brokerage. Feel free to check out IB. I currently park excess cash (yielding 4.5%+ on idle cash) at Interactive Brokers

In our emails, we will provide the following coverage points:

Strongest corporate guidance in two years. Guidance is strongest in Industrials and Health Care (two relatively crowded sectors) and weakest in Tech. As such, S&P 500 2023E EPS has started to bottom, +1% from April lows to $221 after falling 13% since June – BofA expect growth to resume in 3Q.

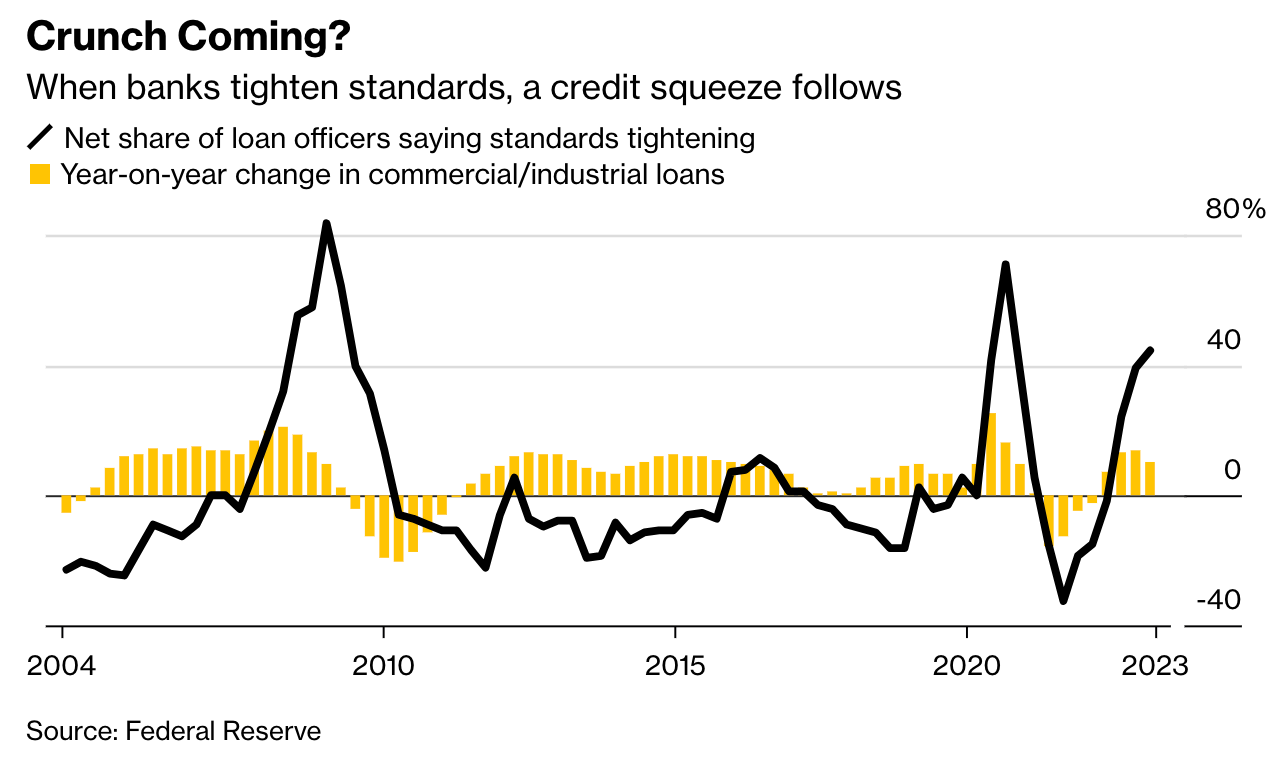

Bank failures intensify the impact of increased interest rates on limiting credit. As evidenced in the previous year, the Senior Loan Officer Survey, which is the Fed's favored gauge, indicated that lending standards were becoming stricter, and this trend is expected to quicken after the SVB incident. Typically, lending slowdowns occur with a delay after banks become cautious, which is one reason to anticipate a downturn in the second half.

Moreover, stresses in the banking system often have a snowball effect. Initial claims that SVB was a unique case now seem inaccurate, as the contagion has spread. In terms of asset size, bank failures in 2023 are already comparable to those in 2008.

During his press conference, Powell described the resolution of First Republic, which was acquired by JPMorgan Chase & Co. last week, as an "important step towards drawing a line" under the crisis. However, the volatility of shares in other regional lenders since then implies that the line is still unclear.

Chart That Caught Our Eye

Analyst Team Note:

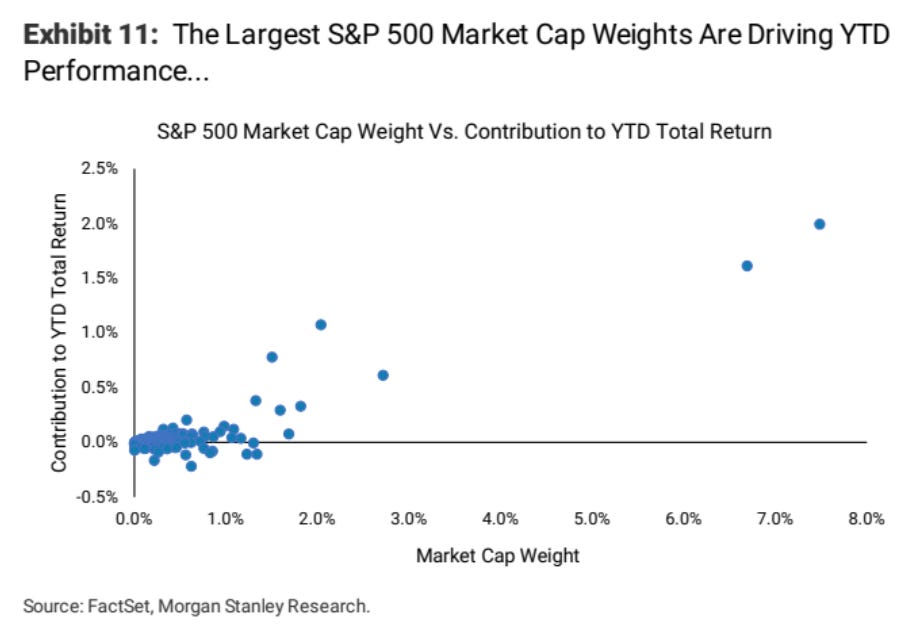

Equity indices have shown resilience, primarily driven by mega-cap stocks. The top 10 index weights have contributed 86% of the YTD total return for the S&P and makeup 28% of the S&P's market cap. These contributions are outsized compared to their 2023 consensus net income weight (22%) and sales weight (17%). While the S&P 500 has held up, buoyed by mega-cap strength, it may not be the most reliable indication that the macro backdrop remains robust.

Sentiment Check

Make sure to check Larry’s most recent market updates via his personal newsletter.