Note to Readers from Larry: As discussed from a recent China Strategy note, the sector was primed for a relief bounce from key support levels. China is an incredible sector for alpha for traders who have key levels prepared and are ready to take near-term positions and exits with discipline. For longer-term pure buy & hold investors, the Sector’s gains need to be treated with incredible caution as they are ephemeral.

Key Investing Resource: Strategist Larry uses Interactive Brokers as his core brokerage. Feel free to check out IB. I currently park excess cash (yielding 4%+ on idle cash) at Interactive Brokers

In our emails, we will provide the following coverage points:

Only a few mega caps leading this rally. The rest suffer.

Macro Chart In Focus

Analyst Team Note:

Is the banking crisis over?

The usage of the Fed's emergency facilities increased again in the latest week, suggesting deposit outflows and funding strains in some banks. Total usage rose to $155 billion from $144 billion. The past week also saw $51 billion of government money fund inflows and $6 billion of prime funds inflows, which nearly offsets the outflows from the previous week, likely due to tax payments.

Reserves in the banking system slipped by $33 billion but remain above pre-SVB levels, possibly due to ongoing QT.

The Federal Reserve is expected to raise interest rates by 25 basis points at the upcoming meeting, followed by a pause in June, with a weak bias towards future rate hikes rather than cuts. The Fed aims to signal an extended hold and counter the market pricing of rate cuts for 2023 and 2024.

The 2Q Senior Loan Officer Opinion Survey (SLOOS) results, which will be available to the Fed during the May meeting, may strengthen the case for a pause in June. However, with two employment and CPI reports between the May and June meetings, the Fed will not completely rule out a June hike in case of strong data surprises.

Chart That Caught Our Eye

Analyst Team Note:

Lots of fear-mongering about U.S. CDS spreads on Twitter from people that don’t know what they’re talking about.

The CDS market is extremely illiquid. Net notional outstanding is only $5 billion and there’s no guarantee the CDS will even pay out if the U.S. somehow defaults. A determination committee under the oversight of the International Swaps & Derivatives Association would ultimately have to decide if the swaps payout.

Also, increases in CDS spreads don’t necessarily equate to a higher probability of default.

More classic fintwit sensationalism.

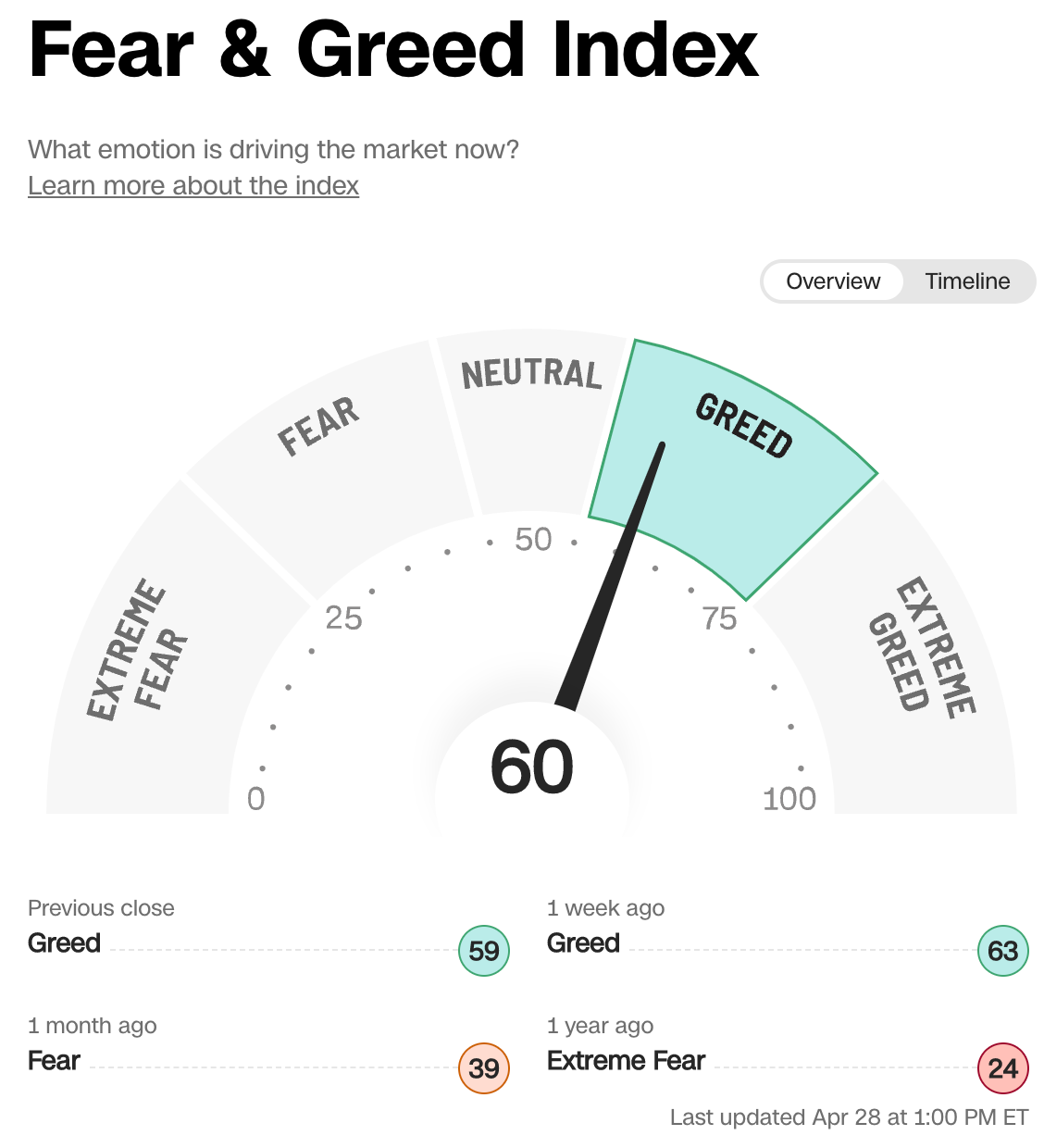

Sentiment Check

Make sure to check Larry’s most recent market updates via his personal newsletter.