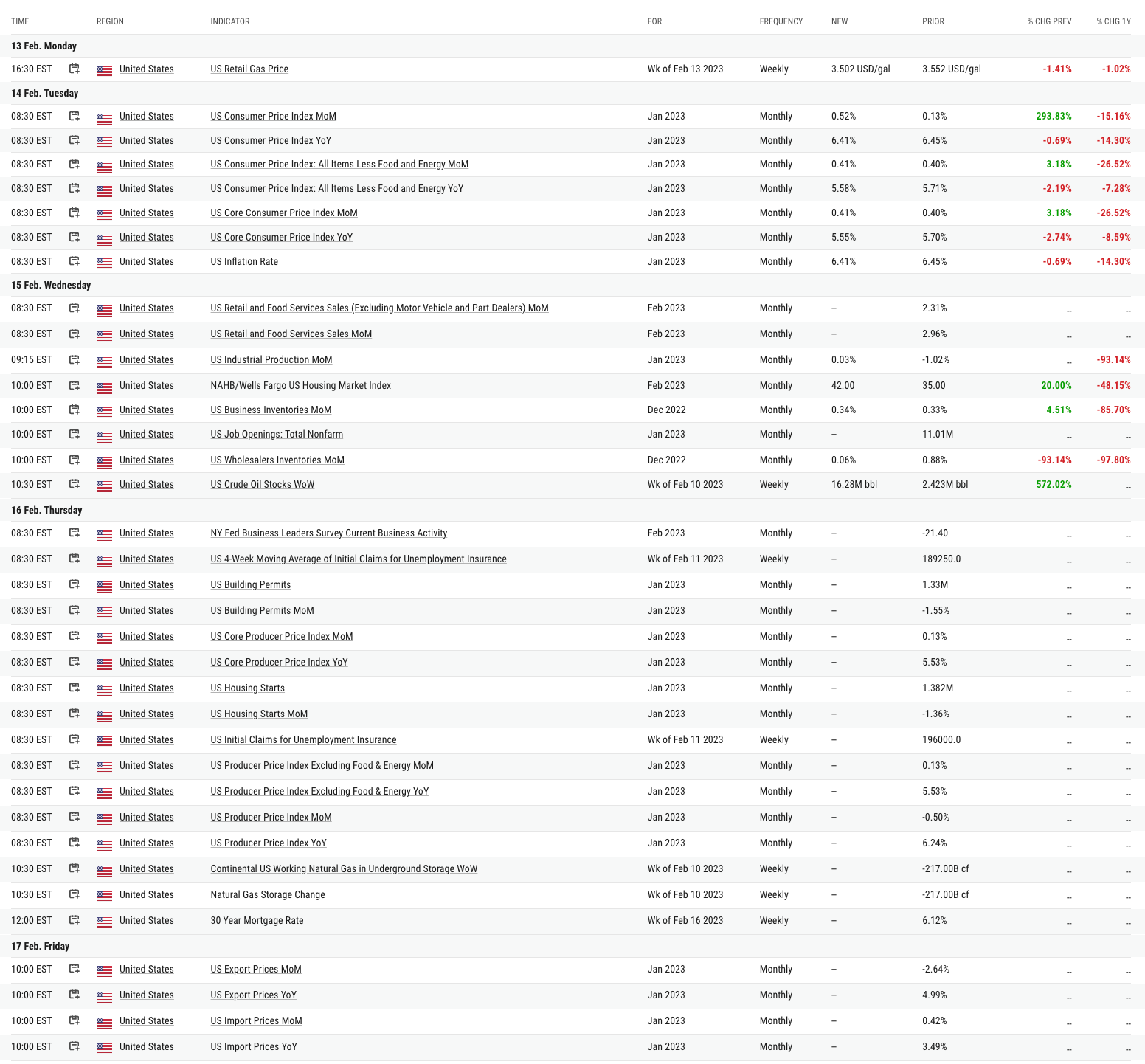

Note to Readers from Larry: I’ll be publishing Part 2 of our Mid-Month strategy report tomorrow (Part 1 is here). The market’s advance and momentum has been unquestionably strong.

However, the U.S. market’s advance is rising in tandem with a rising Dollar and short-term Treasury Yields (the 2Y Yield).

The Bond Market, the Currency Market, and the Precious Metals Market (Gold) all signal that tighter monetary conditions are coming. The Stock Market chooses to ignore this (for now).

I continue to lean on the Bond Market being correct about its assessment of the outlook, and will keep you updated. Make sure to read Part 1 of my mid-month Report if you haven’t yet already. My views are completely unchanged since the Inflation report. An update will be coming tomorrow.

Do I trust the bond market or the current rally in say ARKK ETF to tell me where the S&P 500 is likely heading later this year (a longer-term view)?

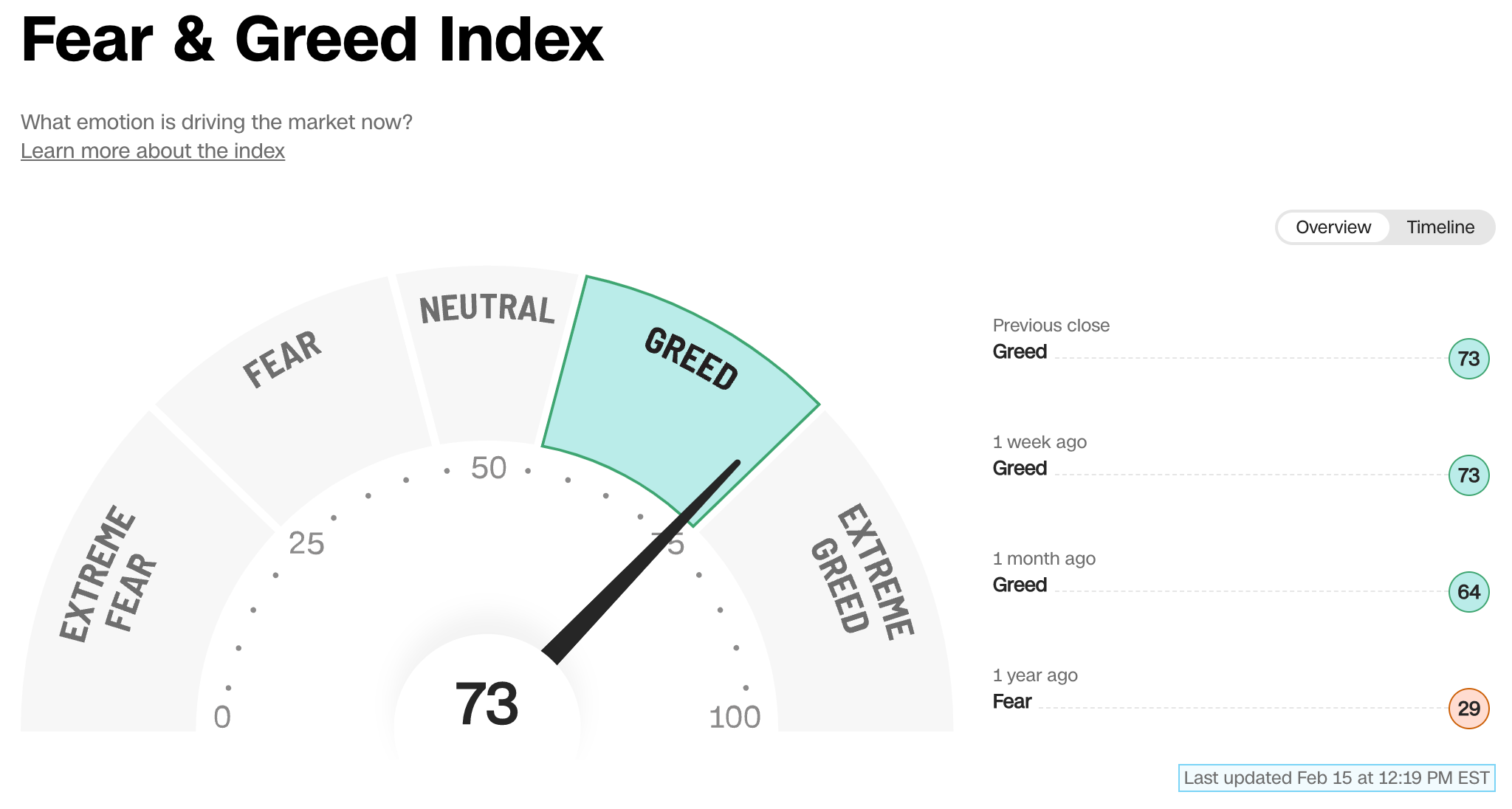

Global fund managers have increased their allocations to emerging market equities, including China, for a third consecutive month, according to a survey by Bank of America. This comes as Chinese blue-chip stocks have risen 14% since November, as investors react positively to President Xi Jinping's decision to abandon the country's zero-Covid policy.

While fund managers are concerned about the rapid increase in the popularity of Chinese stocks, with one in five viewing it as the market's "most crowded trade," some analysts believe that the rally in Chinese equities still has further to run. However, there are concerns that inflation could rise due to China's reopening, which could pose problems for central banks outside China.

The Bank of America survey also found that 46% of fund managers had moved to an "overweight" allocation in emerging market equities in February.

Macro Chart In Focus

Analyst Team Note:

According to research conducted by the Federal Reserve Bank of Atlanta, nearly half of the workers who changed jobs in 2022 in the US were rewarded with pay raises that exceeded the rate of inflation, while only 42% of those who stayed in their position managed to stay ahead of inflation.

The analysis also found that younger workers and job switchers had a better chance of keeping up with inflation than older workers. In 2021, only 38% of employees aged 55 and older saw an increase in their real wages, while 60% of workers aged 16 to 24 received an above-inflation raise.

According to Commerce Department data, US retail sales increased by 3% in January, the most significant rise in almost two years. The figures, which aren't adjusted for inflation, suggest robust consumer demand, particularly in the automotive, furniture, and restaurant sectors, and could bolster the Fed’s commitment to raising interest rates amid persistently high inflation.

Although the report doesn't provide a complete picture of consumer spending, as it only covers goods and services, it suggests that US consumers have bounced back from a spending slowdown at the end of 2022.

Chart That Caught Our Eye

Analyst Team Note:

“An aging demographic impacts supply and demand for credit: people tend to borrow more in the first 40 years or so of their life (to finance education, the purchase of their first home, etc.), and to lend more in the last 40 years of their life (as they pay down debt and build investment portfolios and retirement accounts). As such, demographic aging typically increases the supply of credit available in the economy, while decreasing demand, thereby pushing down the real rate of interest. While the accounting here is rather complicated, the impact is fairly simple – as one can see in Exhibit 27, interest rates tend to be lower for a given level of GDP growth when populations age.” - KKR