2.10.23: Momentum Names Begin To Reprice Risks Ahead of U.S. CPI Inflation Report Next Week. Do not be a Sitting Duck.

For Public: Weekly Key U.S. and China brief market notes by Larry Cheung's Analyst Staff Team for our Public Email List

Note to Readers from Larry: Danger has arrived in momo (momentum) names within QQQ, much to our pleasant surprise as this was highly anticipated in our timely and still very much applicable strategy note to members (please read if you haven’t yet).

When it comes to markets, I now guide on upside and downside expectations. The violent repricing in QQQ components makes sense in the context of my researched observations. Media outlets have dangerously convinced folks that a soft landing is here. That debate is bound to intensify, but I continue to believe that a soft landing is not my base case.

Now, many folks in my social media comments have opined their thoughts such as “markets are forward-looking” or “the negativity is priced in.”

While this of course could be correct, I’ve been in more of the camp that “the good news and soft landing are quite priced in.”

I look forward to continuing this intellectual discussion with you in my Substack/Patreon Investment Community through my research notes. Make sure to follow me on Twitter and Instagram for insightful short-form thoughts and thought-provoking commentary.

Strategist Larry uses Interactive Brokers as his core brokerage.

In our emails, we will provide the following coverage points:

Brief Overview of U.S. & China Markets

Macro Chart in Focus

U.S. & China Upcoming Economic Calendar

Chart That Caught Our Eye

U.S and China Markets Brief Snapshot 🇺🇸 🇨🇳

(Powered by our Channel Financial Data Provider YCharts)

S&P 500 Index: 4081.50

KWEB (Chinese Internet) ETF: $33.12

Analyst Team Note:

Weekly flows: $7.4bn to bonds, $7.4bn from equities, $10.1bn from cash.

Flows to Know:

1st outflow US Treasuries in 11 weeks ($63mn)

more inflows to IG bond ($6.0bn) but pace slowing

EM debt & equity inflows rolling over - 1st outflow EM equities in 8 weeks

largest outflow $3.1bn China equities since Mar’22

stock outflows from Europe resume ($0.7bn)

1st tech inflow in 11 weeks ($1.0bn)

big US small cap big inflow ($1.7bn)

healthcare outflows past 4 weeks biggest since Jan’19

Source: BofA

Macro Chart In Focus

Analyst Team Note:

Despite Cathie Wood’s ARK Innovation ETF declining by 67% in 2022, it still attracted billions of dollars of inflows. Notably, this year’s advance has featured a precarious revival in risky stocks, with gains more pronounced in unprofitable tech and retail darlings.

This is the antithesis to the Fed’s goal of tightening financial conditions. There’s still too much “buy the dip” going on in the markets and thus, the bottom is not in.

Upcoming Economic Calendar

(Powered by our Channel Financial Data Provider YCharts)

U.S Economic Calendar (Upcoming Data Points)

China Economic Calendar (Upcoming Data Points)

Analyst Team Note:

Per Bloomberg, Russia has announced its intention to reduce its oil production by 500,000 barrels per day in the upcoming month, in response to western energy sanctions. This decision has the potential to destabilize the oil market, which has previously been able to withstand disruptions in Russian supplies. The cut in production will add to the supply restrictions imposed by OPEC+, where Saudi Arabia had already led a 2 million barrel-a-day reduction in production last year to support oil prices.

The delegates from OPEC+ have already indicated that they will not take any measures to compensate for the loss caused by Russia's production cut.

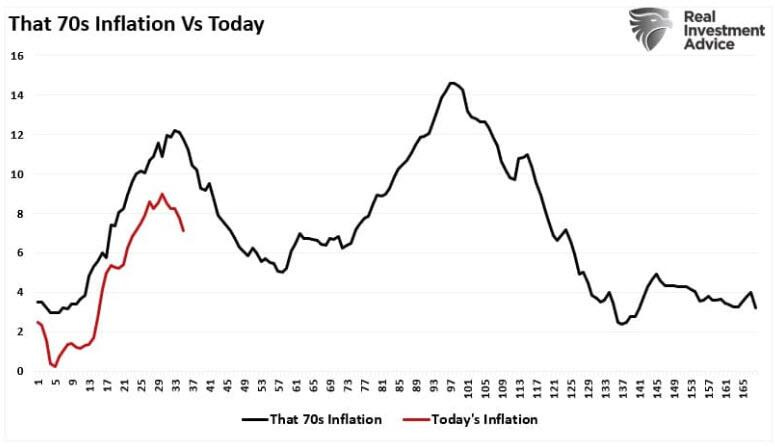

Chart That Caught Our Eye

Analyst Team Note:

“No participants anticipated that it would be appropriate to begin reducing the federal funds rate target in 2023. Participants generally observed that a restrictive policy stance would need to be maintained until the incoming data provided confidence that inflation was on a sustained downward path to 2 percent, which was likely to take some time. In view of the persistent and unacceptably high level of inflation, several participants commented that historical experience cautioned against prematurely loosening monetary policy.” - December FOMC Minutes

Sentiment Check