Note to Readers: As discussed in our February Investment Strategy Part 1 (which you should read), we believed that risk-reward on the long side across most names in our coverage universe was not ideal. Today’s selloff is not a surprise to folks who follow my work closely. And while we could bounce from here, we believe that absent a true soft landing, we are near/close to the upper range of this counter-trend rally.

On specific names: While we still like BABA and TSLA for ultra long-term investment, our call that near-term weakness would arrive soon is now in action. I’ve publicly given many opinions on this, and believe that members are more than prepared for today’s bumpiness. Members should embrace a large pullback rather than fear one.

I believe our commentary has allowed folks to be appropriately positioned. Make sure you’re prepared for what’s to come (read below).

The Nasdaq 100 suffered its worst day since Dec. 22 while the S&P 500 fell the most since Jan. 18.

“Investors seem to have forgotten the cardinal rule of ‘Don’t Fight the Fed. The good news is now priced, and reality is likely to return with month end and the Fed’s resolve to tame inflation.” - Mike Wilson, Morgan Stanley Chief US Equity Strategist

Macro Chart In Focus

Analyst Team Note:

According to the Bloomberg Financial Conditions index, we are “looser” now vs. when we did the first hike, or even when Powell slammed everyone at Jackson Hole. That is consistent with other measures of financial conditions. In the Bloomberg index, we are in outright “easy” territory.

“Mortgage applications are up 28% from early November as the average 30-year-fixed mortgage rate has declined to 6.15% from its November peak of 7.08%—the largest 10-week decline since 2009. That has sent the typical homebuyer’s mortgage payment down 10% (about $180) since fall. Pending home sales rose 3% in December from November on a seasonally-adjusted basis—the first month-over-month increase in 14 months.” - The Housing Market Has Started To Recover by Redfin

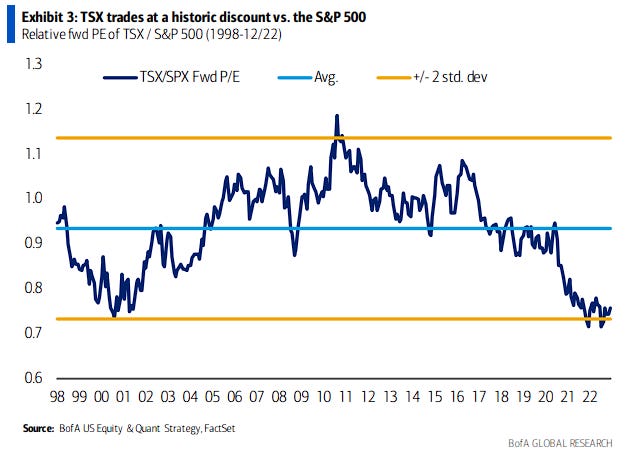

Chart That Caught Our Eye

Analyst Team Note:

“The BoC is clearly being more cautious given the slowdown, which also lowers the risk of a housing crisis, which has been a major bear case for Canada. With a lower discount rate and the risk premium already largely pricing in recession risk (more below), we believe TSX multiples are at trough levels at just 13x fwd P/E, in line with the Tech Bubble low relative to the S&P 500’s 17x.” - BofA

Sentiment Check

Make sure to check Larry’s most recent market updates via his personal newsletter.