Note to Readers from Larry: There are only about 45 days left before the start of a new year in 2023. Based on my observations of macro conditions, I think we still are in a bear market, but the next big leg lower (if there is one) will most likely come in 2023. There are not enough immediate bearish catalysts to drive the market significantly lower into upcoming holiday season, unless the Fed delivers a tremendous surprise in December FOMC*.

The best strategy now is to form a thorough understanding of the changed landscape, where it’s likely heading, and how to position appropriately for the next macro trend in 2023. We’ll be thoughtfully discussing this and more in our future Bi-Weekly reports.

Our latest report from Mid-November cautioned on Semiconductors, especially Lam Research and Applied Materials. If you are invested in Semiconductors, there are certain companies that have greater risk now that Republicans have reinstated their stance on China. If you’re a U.S. or China tech investor, make sure to read the rest of my content on my previous emails. I want to help you succeed. Have a wonderful weekend. For members inside my Community, I’ll check 1:1 messages later this weekend. Please always give me 2-3 days to respond to 1:1 chats because I am constantly researching and strategizing next steps on market risk/reward for the community at-large. Thank you so much.

In the 25 negative years since 1928, the S&P has fallen less than 10 pct just over half the time (56 pct, or 14 years). During these years, the average return was -6.0 pct and the next year the index was positive most of the time (79 pct, or 11 out of 14 years). The average return in the subsequent year was +17.5 pct.

The S&P was down double digits in 11 out of the 25 negative years (44 pct of the time), losing an average of 22.6 pct. The next year it was positive just over half the time (55 pct, 6 out of 11 years) and up by an average of just 6.4 pct.

Source: DataTrek

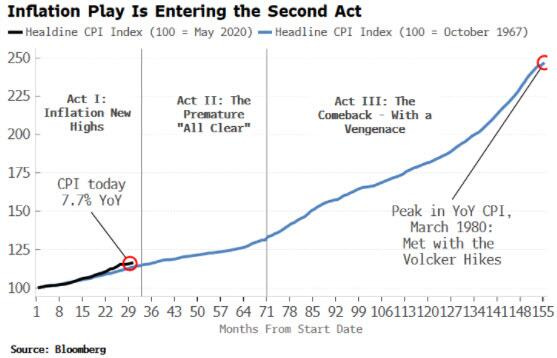

Macro Chart In Focus

Analyst Team Note:

Inflation today is going through one of these [regime] shifts, analogous to the 1970s. In that decade, inflation could be understood as a play in three acts, a drama that is likely to be repeated in this cycle.

In the first act, inflation makes new highs and the Fed tightens aggressively.

The second is when inflation begins to recede, allowing the central bank to pull back from tightening.

The final act is when we see inflation return with a vengeance, eliciting a Volcker-esque monetary response and a deep recession in order to fully snuff it out.

Interesting take from Bloomberg… Full article here.

“While all employment indicators have improved materially on a YoY basis, sequentially, the unemployment rate and continuing jobless claims are softening. Meanwhile, consumer confidence has deteriorated on a y/y basis due to persistent inflation, higher fuel prices, and recession risk. The risk of a hard landing is increasing and driving lower consumer confidence. Additionally, the mortgage backdrop has become progressively more difficult, higher interest rates are leading to lower originations overall and worsening affordability.” - Bank of America

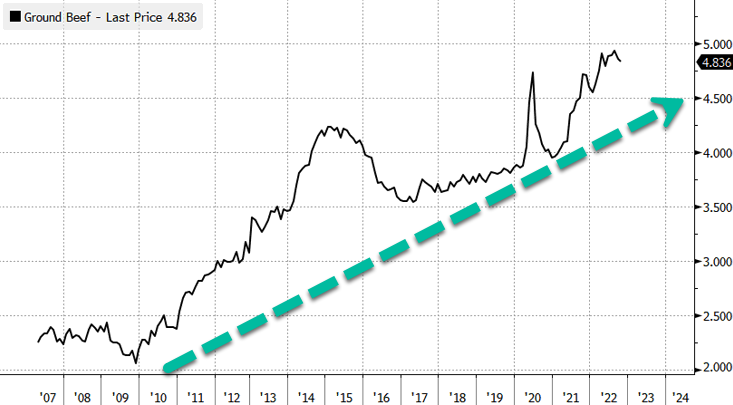

Chart That Caught Our Eye

Analyst Team Note:

Estimates for cattle placed into feedlots is nearing the lowest level since 2012. Per Bloomberg “That's a reversal from recent months, when ranchers faced with dwindling supplies and sharply higher prices for hay moved more animals off the ranch, helping to keep meat supplies relatively plentiful. Fewer animals moving closer to slaughter would signal herds are shrinking, which will likely mean higher meat prices down the road”.

Meat is becoming a luxury… Ground beef prices per pound at the supermarket are up 25% since early 2020 and more than 134% since 2009.

We want to take a moment to thank Interactive Brokers for being one of our Channel’s trusted Partners and to inform my audience of the special features they have given that our online friends here closely follow Chinese Internet stocks (BABA/Tencent).

Much of Larry’s audience is concerned about the US ADR issue of Chinese Stocks being delisted.